Changing Technological Landscape of the Global Energy Sector: Drivers and Opportunities

[Чтобы прочитать русскую версию статьи, выберите русский в языковом меню сайта.]

Viatcheslav Kulagin – head of the Department for Research of the Energy Complex of the World and Russia, ERI RAS.

SPIN-RSCI: 4140-6845

ORCID: 0000-0001-8847-8882

Researcher ID: Z-5621-2019

Scopus Author ID: 56274242400

Dmitry Grushevenko – senior researcher at ERI RAS.

SPIN-RSCI: 7801-4079

ORCID: 0000-0002-8660-2576

Researcher ID: AAD-4257-2019

Scopus Author ID: 57039179500

Anna Galkina – senior researcher at ERI RAS.

SPIN-RSCI: 2474-7057

Researcher ID: M-9885-2013

Scopus Author ID: 56607057900

For citation: Kulagin, V., Grushevenko, D., and Galkina, A., 2024. Changing Technological Landscape of the Global Energy Sector: Drivers and Opportunities. Contemporary World Economy, Vol. 2, No 2.

Keywords: technologies in the energy sector, inter-fuel competition, renewable energy sources, LCOE, energy storage, scientific and technological progress.

Abstract

The article provides an overview of the key expected changes in the technological landscape of the global energy sector. On the part of the end-use energy consumption sectors, the requirements for energy systems and the organization of their operation are changing significantly. Consumers are demanding ever more versatile, environmentally friendly, cost-effective and reliable energy supplies, and energy-intensive equipment with off-grid options is increasingly in demand. Technical progress, in turn, provides access to new solutions, while changing the parameters of inter-fuel competition. Government policy also contributes, and its tools allow both to softly influence the attractiveness of the choice and to simply limit the possibilities of using certain equipment.

Electrification is becoming a key trend in the supply of energy to industry, commercial and residential sectors. The transportation sector is moving from an era of oil dominance to an era of inter-fuel competition, with electric solutions also becoming a key substitute for petroleum products.

In the electricity generation sector itself, preference is increasingly being given to carbon-free and renewable energy sources. In some regions of the world, renewable energy sources are already becoming competitive in terms of the cost of electricity production (before feeding into the grid) with fossil generation. It is important that with an increase in the share of renewable energy sources in the electricity balance, the share of costs for backup, storage, and network infrastructure increases, which makes it necessary to assess costs in a complex manner when making decisions.

The growing share of renewable energy sources in energy systems necessarily requires the development of storage technologies; however, the current level of scientific and technological progress in this area makes such solutions extremely expensive, which leaves long-term niches for thermal generation, but significantly changes its operating modes.

Technologies are also changing significantly in the field of exploration, production and transportation of fossil fuels. This makes it possible not to fear resource shortages in the coming decades, despite rising production levels and the depletion of the easiest-to-exploit reserves. But the operating environment for conventional energy will change.

Introduction

The energy sector is currently undergoing a period of substantial technological transformation. This transformation is driven by a confluence of factors, including the advent of novel opportunities propelled by scientific and technological progress, the increasing complexity of the resource base, escalating requirements for the quality and options of energy supply from end consumers, and the influence of government policy.

In every sector of the energy end-use sector, novel solutions are emerging, and the field of inter-fuel competition is expanding.

The array of prospective technologies is extensive and continuously expanding. However, the race to develop these technologies will be won by those who can effectively prioritize and allocate financial and scientific resources to segments that will be in practical demand in the future. History demonstrates that even the most promising technologies, initially poised to transform the global energy industry, have often occupied limited niches in the market or remained theoretical, encountering unforeseen challenges. A notable example is the series of accidents at nuclear power plants (NPPs), which have led to a re-evaluation of the peaceful atom, a technology that was projected to account for 80% of the world’s energy production by the 2020s. Difficulties in development and high costs of gas hydrates extraction have left them at the level of experiments instead of 10% share in the world balance by 2025.

High production costs and technological challenges have hindered the realization of plans to develop Helium-3 on the Moon. Furthermore, concerns regarding food security and the concomitant environmental impact have impeded the substantial displacement of petroleum products by biofuels in engines. For a comprehensive overview of technologies that have fallen short of expectations, refer to [Kulagin 2020].

The development and testing of many technologies require decades of investment and research before a prototype is ready for market implementation. The timeframe for market penetration varies significantly depending on the specific segment. For instance, a novel battery type intended for cell phones or tablets is projected to be adopted in 50% of devices within a few years following the commencement of the commercialization process. In contrast, the large-scale implementation of a novel oil refining process is estimated to require 25–30 years, while a new nuclear reactor is anticipated to take 50–60 years. The temporal framework is defined by the rate of equipment and infrastructure upgrades within each segment [Kulagin 2020].

In the context of the power industry, characterized by protracted investment cycles and extended planning horizons, it is imperative to identify the technologies that are likely to be predominant and widely demanded by the year 2050. This underscores the necessity for comprehensive review studies that seek to elucidate the pivotal drivers of energy system transformation and to identify optimal solutions from among the available options.

1. Changing energy end-use technologies: Consumer demands and regulatory constraints

Consumer demands on energy systems, household processes, and the performance of the appliances that serve them are increasing on a continuous basis. The following are a few examples:

-Saving time, a commodity that is widely considered the most valuable resource in modern life, is of particular importance. By acquiring a robot vacuum, dishwasher, or washing machine, we gain time, allowing us to allocate our time toward more fulfilling activities.

-Cost-effectiveness and environmental impact. When buying appliances, we often strive for rational consumption, choosing between the initial cost and the costs of operation. Consequently, a refrigerator of A+ energy class, which is initially more expensive, will reduce energy consumption more than twice as much as a model of C class and will be cheaper in terms of total costs during its lifetime. Furthermore, consumers have expressed a growing interest in appliances that are environmentally sustainable, emphasizing the materials used in their production and the methods employed during operation.

-Convenience. As prosperity increases, prices become a less significant factor in purchasing decisions. The emphasis has shifted towards the convenience of utilization, with features such as self-cleaning mechanisms (refrigerators, ovens, vacuum cleaners) and portable operation (without the need for constant repositioning of cords) being highly sought after.

-Intelligence and controllability. The demand for smart devices, including those that can be remotely controlled via the Internet, is increasing. This demand is evidenced by the proliferation of remote-control systems for indoor climate control, automated cooking, affordable video surveillance, baby monitors, and smart speakers. These devices, when first introduced to the user, can create a new demand for energy.

-The power and operating time of the devices to be charged are also critical factors. This parameter is also often a crucial factor in consumer electronics selection. Phones, laptops, tablets, and electric scooters with extended battery life are experiencing heightened demand.

-Universalization. The demand for uniformity in connector ports, sockets, and plugs is not merely a consumer trend but often a response to regulatory requirements. For instance, by the end of 2024, all mobile devices sold within the European Union (EU) must be equipped with a Type-C connector, as mandated by the EU Parliament in 2022. This trend is not exclusive to consumer electronics. In rural areas, for instance, propane stoves, wood-fired furnaces, and diesel generators are common sources of electricity, underscoring the need for constant oversight of energy resources. A significant number of individuals express a desire to transition to a unified energy source capable of powering all domestic systems.

-Sustainability of energy supply. Consumers seek a reliable energy source to avoid the potential loss of essential energy during times of crisis.

-Autonomy. Temporary departures, the development of new territories, and the energy demands of consumers residing in remote areas far from centralized infrastructure necessitate the exploration of optimal solutions for autonomous energy supply.

The demands of consumers in the commercial and residential sectors are also influencing the requirements for energy supply. The predominant trend in this regard will be the escalating demand for electrification and energy storage solutions.

The advent of technological advancements has given rise to an expanding array of alternatives and a growing field of inter-fuel competition in the domains of space and water heating systems. In most cases, the utilization of gas and coal remains the most economic option. In the case of centralized district heating and electricity supply, this option facilitates enhanced efficiency through the effective utilization of residual heat. Concurrently, the appeal of electric devices of various types is also increasing, both for additional heating and for creating more comfortable conditions in locations where centralized systems are not feasible (e.g., warm floors, entrance areas). A particular focus should be placed on autonomous facilities that are not connected to centralized heating systems or gas networks. In this regard, a wide array of options is available. If electricity is available, it emerges as a highly advantageous solution. However, there are also options for achieving complete autonomy, including gasoline and diesel generators, gas installations using liquefied petroleum gases (LPG) and methane (in gaseous or liquefied form), coal and wood stoves, and novel technologies such as solar panels, heat pumps, and biogas. The selection of a particular energy source is contingent upon considerations such as physical accessibility, cost, and environmental impact.

When consumers purchase vehicles, they typically prioritize various indicators, with manufacturers striving to offer more attractive solutions. These indicators include the cost of operation, which encompasses the vehicle price, maintenance, and refueling costs; acceleration dynamics; mileage without refueling or recharging; comfort; quality of multimedia systems; and reliability, defined as trust in the brand and technologies used. An increasing focus on environmental sustainability by consumers and regulators is also a salient trend. The accessibility of service and refueling/charging infrastructure constitutes a pivotal criterion in the selection process. This shift is precipitated by evolving lifestyles, the aspiration to enhance daily comfort, and the advent of new technologies, such as individual small mobility solutions (electric scooters, electric bicycles, monocycles), delivery robots, and drones. In this context, electrification emerges as a pivotal trend, akin to its role in the utility sector. The inter-fuel competition field is expanding in all modes of transportation. For road transportation, the competition is between petroleum products, natural gas, biofuels, electricity, and hydrogen [Kulagin et al. 2020]. For railway transportation, the competition is between petroleum products and electricity [Grushevenko et al. 2023]. For maritime transportation, the competition is between petroleum products, ammonia, methanol, biofuels, and even nuclear facilities [Grushevenko et al. 2023].

In industry, the demands on energy supply technologies are also changing. Traditionally, the sector has followed three basic principles when selecting an energy resource: energy must be cheap (to reduce production costs), safe, and the energy carrier must be supplied sustainably (for process continuity). Now new guidelines are being added to these ones:

- Image of the energy component. Manufacturers often choose not the cheapest, but the most environmentally friendly solutions, monetizing their ESG-values in the growth of the value of their own shares [Deloitte 2023]. But in many cases, this choice has a point demonstration character, without large-scale re-equipment of all production facilities.

- Autonomous energy supply—the ability to provide energy for production remote from the grid infrastructure in new territories.

- Quality of energy source—modern equipment becomes more demanding of the energy source (class of oil products, compliance of electricity parameters with established values, etc.).

- Optimizing tax payments. Carbon taxation and carbon border barriers are forcing some producers of energy-intensive products to consider the source of their energy supply.

Against the background of the development of automation and robotization of technological processes, the demand for electricity is also increasing in the industrial sector.

In addition to consumer requirements, government policy has a significant influence on the set of energy supply options in each sector, which allows adjusting consumer demands and the attractiveness of using specific solutions. Among the most prominent examples:

- Tariff, tax and price regulation that artificially inflates the cost to the consumer of some solutions and lowers the cost of others.

- Energy efficiency standards favoring specific technological schemes for buildings, equipment, industrial plants, etc.

- Fuel class requirements

- Direct bans and restrictions—g., banning the use of light bulbs, sale of certain containers, banning internal combustion engine vehicles from entering city limits, etc.

- Direct and indirect subsidization of energy supply—g., connection to the electricity grid or to gas not at the expense of the consumer or through co-financing schemes.

- Carbon regulation.

The set of applied tools can significantly adjust the initial demand formed by consumers for the energy supply system and the consumption level itself.

In the future, inter-fuel competition will continue to expand, and demand for electric power in end-use sectors will grow faster than for any other type of energy carriers, which is well seen in the forecasts of ERI RAS [Makarov et al. 2024], the International Energy Agency [IEA 2023], OPEC [OPEC 2023], and others.

Thus, the main battlefield for fuel alternatives is becoming the electric power generation segment, and its technological landscape will largely determine the future of the global energy industry.

2. Electricity generation: Renewable or fossil?

In the domain of power generation, a pivotal concern pertains to the prospective parameters of inter-fuel competition among conventional fossil-fueled generation, nuclear power, and renewables. In 2021, renewable energy sources (RES) contributed up to 15% of the global primary energy consumption. Approximately half of this energy was utilized directly in end-use sectors. The primary end-use sectors for this energy were heating and cooking, with biomass and waste being the main sources. The remaining half was allocated to electricity generation. Of this, 40% of generation came from hydropower, 25% from bioenergy (biogas, solid biomass, waste), and the remaining approximately one-third from new RES (solar power plants (SPPs), wind power plants (WPPs), geothermal plants (GPPs), ocean energy, etc.) [IEA 2023]. Concurrently, it is the new RES that have exhibited the most substantial growth rates over the past decade, and it is with these that the primary expectations for the transition to a novel energy sector are associated. However, the viability of these prospects is contingent upon the specific characteristics of STP in each segment.

In the domain of solar energy, crystalline silicon photovoltaic plants (PVs), which directly convert sunlight into electricity through photovoltaic cells, are currently the most prevalent. Since 2010, the cost of these facilities has decreased from 0.43 $(2023)/kWh to 0.08 $(2023)/kWh. This decline has led to a situation where, in certain regions, the cost of solar energy is comparable to that of traditional energy sources in terms of the cost per kilowatt-hour produced. The reduction in costs has been achieved primarily through the expansion of production facilities and the relocation of manufacturing operations from OECD countries to developing Asian countries, where labor and critical materials utilized in panel production are substantially more affordable. While the technology’s learning curve has largely been surmounted, there remains potential for further cost reductions through reductions in cell thickness, increases in lifetime, and optimization of module architecture [VDMA 2022; DNV 2023; AEGIR 2022].

The potential for breakthroughs in photovoltaics is associated with perovskite technologies (pure perovskite/perovskite-silicon tandem), which are currently under development in Russia [Akbulatov et al. 2017]. The prototypes of these panels exhibit high efficiency, and their production is less costly than that of traditional silicon panels. However, the issue of the material’s extremely high degradation rate remains unresolved, with the longest achieved lifetime being one month. In contrast, silicon panels face the challenge of uneven generation. The maximum efficiency of silicon panels is observed under specific insolation parameters, and cloudy or excessively hot weather hinders the attainment of optimal operating conditions. A persistent challenge in solar energy generation pertains to the lack of output after sunset, accompanied by a substantial decline during periods of precipitation, overcast conditions, and the winter season.

Theoretically, the issue of nighttime generation can be addressed by concentrated solar power (CSP) technologies. In such systems, the sun’s rays are reflected from heliostat mirrors and heat up a tower located in the center of the station, where a coolant heated to a temperature of 600 degrees Celsius is stored. In the absence of sunlight, the tower functions as a conventional thermal power plant, converting thermal energy into electrical energy for an extended period of a few hours. However, these systems are associated with significant disadvantages (in addition to the fact that they are 2 to 3 times more expensive than conventional crystalline panels in terms of the cost of energy production [IRENA 2023a]), including the need for extensive land areas and the requirement for substantial resources such as fresh or desalinated water, which are necessary for the technological processes involved.

Wind farms represent another prevalent category of renewable energy sources. Over the period from 2010 to 2022, there was a significant decrease in the levelized cost of electricity generation (LCOE): from $0.11/kWh to $0.07/kWh for onshore wind power plants and from $0.20/kWh to $0.11/kWh for offshore wind power plants. According to the expert community, the prospects for further cheapening of mainland generation through improvements in rotor systems and blade materials are estimated to be within 10% [ETIP WIND 2021; DNV 2022]. Conversely, the potential for cost reduction in offshore wind power plants is projected to be more pronounced, with a range of 30–40%, primarily attributable to the anticipated augmentation in turbine unit capacity and the optimization of control and transmission systems [AEGIR 2022; Makarov 2020].

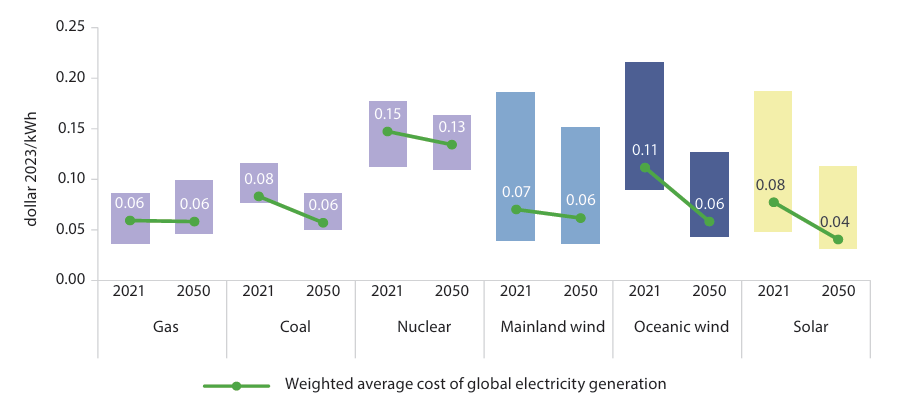

Already, in some regions of the world, PV and WPP generation is competitive with conventional generation in terms of cost per unit of energy (LCOE). In the future, given the projected cost reductions, the attractiveness of RES should increase (see Figure 1).

Figure 1. Projected change in the levelized cost of electricity generation (LCOE) by source in 2050 compared to 2021

The columns show the range of electricity generation costs by region of the world.

Source: ERI RAS calculations.

However, the complexity of a power system extends beyond the mere objective of generating electricity in an economical manner. As electricity travels from the generation source to the consumer, additional costs are incurred, including transmission, storage, distribution, maintenance of reserve capacity, and dispatching. In an effort to account for system effects, certain studies have proposed a shift from the LCOE to the VALCOE of the present unit cost of electricity generation [Karn et al. 2022; Moses 2023].

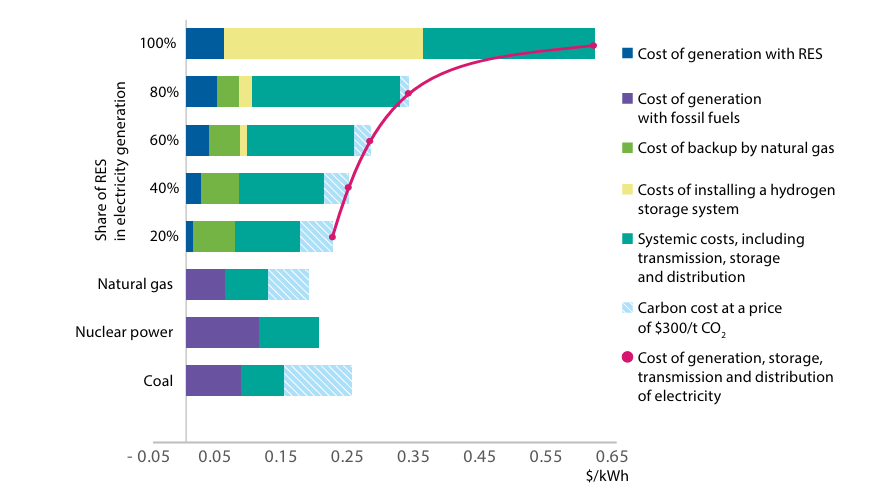

The primary challenges associated with renewable energy generation pertain to the disparity between electricity demand and generation peaks, as well as the substantial reliance on meteorological conditions. For instance, solar panels are unable to meet evening demand, and in cloudy or very hot weather, generation may fail during the day as well. In many regions of the world, generation experiences a significant decline during winter months. Additionally, wind generation exhibits similar challenges, with periods of high output during nighttime hours, but a complete cessation of electricity production during periods of low wind speeds or high wind speeds. Observations of wind power in the EU demonstrate that generation failures can persist for weeks. To address these challenges, the implementation of renewable energy generation systems necessitates either a robust and reliable backup system or an accumulation and subsequent return of generated electricity to the grid. Furthermore, as the share of renewable energy in the energy portfolio increases, the backup costs are expected to rise, given the rising cost of generation at conventional plants as the installed capacity utilization factor (ICUF) decreases. Furthermore, the costs associated with electricity accumulation are subject to a multiplicative increase when considering not intraday modes (e.g., day/night charging, morning and evening peaks of output) but rather reserve capacity for extended periods of a few days, necessitating significantly larger capacities and a very low number of operation cycles during the year. In essence, as the share of new RES in generation increases, system costs escalate disproportionately, a phenomenon that holds true for all countries worldwide (see Figure 2). The specific level of costs is contingent on resource availability, the initial electricity generation mix, natural and climatic conditions, the ability to balance flows with neighboring countries, and numerous other parameters. In cases where the generation is exclusively from renewable sources (i.e., 100% RES), the only viable solution to address long-term generation discrepancies is to convert electricity into another form of energy for storage, particularly hydrogen. However, such approaches are characterized by substantial expense, stemming from the costs of equipment (e.g., electrolysis plants, hydrogen storage facilities, and fuel cells) and energy losses during conversion [Kulagin et al. 2023]. A comparison of hydrogen systems reveals an efficiency range of 25–45% for the cycle “production – charge – discharge – supply to the grid,” while chemical batteries demonstrate an efficiency of 85–95% [Environmental and Energy Study Institute 2019]. Notably, the cost of hydrogen storage (LCOS) exceeds $300/MWh, compared with $150/MWh for chemical current sources [Lazard 2023]. In addition, the utilization of hydrogen entails specific safety imperatives.

Figure 2. Schematic ratio of the full pre-tax cost of electricity supply, taking into account generation costs, system effects, CO2-eq. emission charges for different energy sources

Source: ERI RAS.

It is imperative to ascertain whether there exist alternative methods of generating energy from renewable sources that possess sufficient maneuverability to circumvent the disadvantages inherent in PVs and WPPs. In principle, the answer is affirmative. These include technologies that harness oceanic energy, such as bottom turbine generators driven by strong tidal currents, buoy generators that utilize constant wave energy, and plants that operate through ocean thermal energy conversion, leveraging the temperature difference between the ocean bottom and surface [Lewis et al. 2011]. To a lesser extent, tidal range dam stations can be attributed to such technologies, since they operate only at high tide. However, in terms of levelized cost of energy (LCOE), all “oceanic” solutions are significantly more expensive than WPPs and SPPs (see Table 1), not to mention conventional generation. Furthermore, the environmental implications of these technologies, particularly their impact on marine flora and fauna, have not been thoroughly investigated.

Table 1. Key technologies using ocean energy to generate electricity

|

Technology |

Workout stage |

LCOE 2023, $2023/kWh |

LCOE 2050, $2023/kWh |

|

Tidal range (dam stations) |

Commercial stations are in operation |

0,11-0,24 |

0,11-0,24 |

|

Tidal currents (bottom turbine generators) |

Pilot projects are being developed |

~ 0,9 |

< 0,14 |

|

Wave energy conversion (buoy generators) |

Pilot projects are being developed |

~ 1,024 |

< 0,21 |

|

Ocean thermal energy conversion (OTEC plants) |

There are experimental stations |

~ 0,26 |

~0,13 |

Source: IRENA 2023b, European Commission 2021, ETIP OCEAN 2020.

An alternative to oceanic solutions that has been employed by humankind for over a century is hydroelectric power plants. The procurement of electricity from substantial hydroelectric power plants (HPPs) is comparatively inexpensive, with costs starting from 0.02 $(2023)/kWh. In certain countries, these facilities are the predominant source of electricity generation, with examples including Norway, where hydropower accounts for over 90% of the total electricity production [IEA 2023]. However, globally, hydropower plants currently contribute only 15% of electricity generation and 8% of primary energy consumption [IEA 2023]. The development of hydropower is constrained by several factors, including the limited hydro potential observed in many countries, the geographical dispersion of hydropower resources and consumption centers, and the need for specific landscape conditions for installation. Criticisms of hydropower are manifold, particularly with regard to the disruption of ecosystems within the flood zone. Conversely, there is a growing interest in mini-HPPs and micro-HPPs, which, in theory, can be located even on small flowing water bodies. However, these systems frequently demonstrate unstable output and are often cost-prohibitive, with the LCOE for micro-hydropower plants starting at an average of 0.13 $(2023)/kWh on a global scale [IRENA 2023a].

Another viable option is the utilization of geothermal energy, which is already widespread in suitable locations (geysers, hot springs, etc.). New generation geothermal systems that utilize energy from great depths by drilling deep wells are also being considered. However, the cost of electricity generation using such technologies currently exceeds $0.45/kWh. The viability of these solutions is contingent on the geothermal gradient, defined as the temperature variations at varying depths from the Earth’s surface. The earlier a transition to high temperatures can be achieved, the higher the probability of a plant entering the zone of economic efficiency.

The high cost of some renewable energy technologies and the inadequacies of others in terms of unpredictable output dynamics, against the backdrop of a reinvigorated low-carbon agenda, are driving renewed interest in carbon-free nuclear energy. Nuclear power generation frequently incurs a higher LCOE compared to other carbon-free alternatives. It necessitates substantial capital investment and unprecedented safety measures, surpassing those of other generation methods. However, unlike WPPs and SPPs, nuclear power plants can operate without generation dips and exhibit sufficient intraday balancing capabilities. This results in substantial savings on backup and storage systems compared to renewable energy systems. However, even in this context, the need for backup capacities or the utilization of energy storage remains paramount, necessitating a comprehensive analysis of the energy storage technologies available.

3. Energy storage technologies

Storage technologies are important not only for balancing carbon-free power generation but also for the electrification of end-use sectors: they are used in consumer electronics, off-grid power supply systems, transportation, etc. Despite the wide range of energy storage solutions available, they can all be categorized into:

- Physical systems. In these, the electricity coming from a generation source is converted into kinetic, potential, or thermal energy and then back into electrical energy. Such storage systems include: pumped storage power plants, thermal storage, compressed air systems, flywheels.

- Electrochemical systems. They store and then release electricity through a chemical reaction. These include: alkaline batteries, lead-acid batteries, lithium-ion batteries, redox vanadium batteries, etc.

- Hydrogen systems. These produce pure hydrogen through the electrolysis of water, which is subsequently fed to a fuel cell to generate electricity.

- Electrical—supercapacitors and superconductors. They store and release electricity without converting it.

- Chemical-thermal systems. In these systems, electricity is converted into fuel (synthesis gas or hydrogen), which is then burned.

Concurrently, five predominant sectors have been identified that are influencing the demand for electricity storage. Each of these sectors is expected to witness competition among various storage technologies, each with its own distinct set of parameters. It is noteworthy that in numerous instances, cost considerations do not serve as the primary determinate. Dimensions, number of charge/discharge cycles, charge rate, and runtime may prove to be more significant factors in selection decisions. In the context of electricity storage, the specific application and the necessity of redundancy are also crucial factors. The viability of daytime operation or high-volume storage over extended periods is a key consideration.

- The segment of large balancing power systems. This segment is particularly crucial in mitigating the discrepancies in renewable energy generation. The pivotal parameter in this context is the normalized cost of energy storage, given the commercial orientation of such projects. Another salient parameter is compactness, defined as the ratio of occupied area to storage capacity. The service life of these facilities is also a critical factor, as they are designed to be integrated into urban infrastructure over the long term. Additionally, energy losses per charge/discharge cycle must be considered.

- The segment of consumers relying on uninterruptible/standby power supplies in emergency situations is particularly sensitive to the initial cost of the storage device. The device may only operate a limited number of times during its lifetime if the power supply is uninterrupted, thereby negating the relevance of the LCOS indicator for such systems. The operating temperature range is a critical factor, as uninterruptible power supplies may be necessary in extreme climatic conditions.

- Energy-intensive portable electronics, including cell phones, tablets, electric toothbrushes, and other standalone appliances, are prime candidates for this technology. The storage device must be lightweight and compact, as well as provide maximum uptime at a reasonable price.

- The storage segment for small mobility devices, including electric scooters, monocycles, drones, delivery robots, and warehouse forklifts, among others, is another area of concern. The cost of the storage device is a salient factor in this context, and it is imperative that the cost of the device does not have a significant impact on the overall cost of the equipment. The specific power output is also of significance, as the battery must provide a sufficient range of travel within a compact size.

- The segment of storage devices for electric-powered vehicles (e.g., electric cars, electric buses, electric river streetcars) is sensitive to the cost of the storage device (expressed as the present value of the battery per charging cycle over the vehicle ownership period), as well as the compactness of the battery and the recharge rate.

The key parameters that are important in deciding which drive to choose in each segment and the prospects for changes in these parameters through 2050 are summarized in the tables (see Tables 2 -6).

Table 2. Key characteristics of energy storage technologies for balancing systems in the power industry

|

|

LCOS, $2023/MWh |

Compactness of the system, m cub./MWh |

Service life in charge-discharge cycles and years |

Efficiency per cycle of accumulation-release, % |

|

|

2023 |

2050 |

||||

|

Pumped-storage hydroelectricity |

105 |

100 |

500-5000 |

30-60 years |

70-85 |

|

Gravity |

350 |

315 |

>100 |

30 years |

70-80 |

|

Thermal |

211 |

180 |

5-15 |

30 years |

50-60 |

|

Flywheels |

620 |

555 |

13-50 |

20 000-100 000 cycles (more than 50 years) |

70-85 |

|

Compressed air |

230 |

200 |

150-500 |

20-40 years |

40-50 |

|

Lead-acid |

881 |

724 |

10-15 |

500-600 cycles (1-2 years) |

85-95 |

|

Li-ion |

175 |

135 |

1-5 |

1000-8000 cycles (3-20 years) |

85-95 |

|

Na-ion |

230 |

120 |

3-5 |

~5000 cycles (15 years) |

85-95 |

|

VO-flow |

315 |

205 |

25-50 |

~20 000 cycles (up to 60 years) |

70-80 |

|

H2 fuel cell |

350 |

250 |

1-2 |

5-30 years |

25-45 |

|

Hydrogen-to-power |

400 |

350 |

n/a |

20-40 years |

25-40 |

|

SNG-to-power |

450 |

380 |

n/a |

20-40 years |

20-30 |

|

SMES (Superconducting magnetic energy storage) |

More than 3,000 |

More than 2,000 |

>100 |

20-30 years |

over 95 |

Source: compiled by the authors.

Table 3. Key characteristics of energy storage technologies for consumer-side storage (in the uninterruptible / backup power supply segment)

|

|

Unit cost of capacity, $2023/kWh |

Service life of the system, years |

Optimum operating temperature range, 0C |

|

|

2023 |

2050 |

|||

|

Lead-acid |

90 |

90 |

3-5 |

+15... +25 |

|

Li-ion |

120-400 |

95-300 |

~ 10 |

0...+40 |

|

Na-ion |

151 |

65 |

10-15 |

0...+40 |

|

NiCd |

350 |

350 |

Up to 20 |

-20...+40 |

|

VO-flow |

650 |

430 |

20-30 |

+10...+40 |

|

H2 fuel cell |

750 |

550 |

Up to 30 |

0...+80 |

|

Flywheels |

1500 |

1350 |

Up to 30 |

Theoretically unlimited |

Source: compiled by the authors.

Table 4. Key characteristics of energy storage technologies for energy-intensive portable electronics

|

|

Specific energy intensity, W·h/kg (volume of energy contained in a unit of mass) |

Average unit mass cost per unit of capacity, $2023/g (cost per unit mass) |

Full charge cycle time |

||

|

2023 |

2050 |

2023 |

2050 |

||

|

Li-ion |

200-300 |

250-350 (potentially more than 1,000) |

0,45 |

0,35 |

5-60 min. |

|

Na-ion |

80-120 |

100-150 |

0,65 |

0,45 |

20-60 min. |

|

NiCd |

40-60 |

40-60 |

7 |

7 |

4-6 hours |

|

NiMH |

140-300 |

140-300 |

2,75 |

2,75 |

4-6 hours |

Source: compiled by the authors.

Table 5. Key characteristics of energy storage technologies for small mobility vehicles

|

|

Specific cost of capacity unit, $ per unit 2023/kWh |

Specific power, W/kg |

||

|

2023 |

2050 |

2023 |

2050 |

|

|

Lead-acid |

90 |

90 |

100-250 |

100-250 |

|

Li-ion |

141 |

110 |

200-500 |

250-800 |

|

Na-ion |

150 |

65 |

100-200 |

150-300 |

|

NiMH |

550 |

550 |

250-1000 |

250-1000 |

Source: compiled by the authors.

Table 6. Key characteristics of electricity storage technologies for autonomous transportation

|

|

Levelized value of the battery per cycle, $2023/charge-discharge cycle |

Weight of standard battery*, kg |

Full charge cycle time |

|

|

2023 |

2050 |

|||

|

Li-ion |

28 |

25 |

150-700 |

5-60 min. |

|

Na-ion |

30 |

13 |

350-700 |

20-60 min. |

|

NiMH |

111 |

111 |

200-400 |

4-6 hours |

|

Lead-acid |

20 |

18 |

1100-1800 |

6-8 hours |

* The average electric vehicle battery has a capacity of 55 kWh

Source: compiled by the authors.

In almost all segments, lithium-ion batteries are among the best solutions, which makes it safe to call lithium the new gold. However, in case of metal shortages and a significant increase in the cost of lithium-based batteries, interest in alternative solutions, such as sodium-based batteries, will also increase. That said, most storage solutions are still quite expensive. Therefore, in the power sector, the rational solution for balancing RES in terms of energy availability is backup at the expense of conventional generation.

4. Fossil fuel production and supply technologies

The depletion of the most accessible deposits and the increasing competition among fuels in the power sector and end-use sectors are stimulating STP in the production, supply, and processing of fossil fuels. The achievements of related sciences: IT, chemistry, physics, materials science, etc., are widely used in this process.

Across all elements of the production chain, efficiency can be improved by implementing smart and digital solutions. This includes reservoir modeling, smart drilling, intelligent pipeline flow control, digital filling stations, and other segments. With the use of sensors and robotic inspection systems, it is possible to detect malfunctions in a timely manner and prevent accidents. Digital twins are increasingly in demand for working out project variants before operation, testing abnormal situations and software, and training specialists. The development of the unmanned aerial vehicle industry provides new opportunities for monitoring fields and pipeline routes (visually and with the use of diagnostic equipment), conducting geological exploration, and ensuring the delivery of cargo to remote locations. Artificial intelligence algorithms capable of processing large amounts of data are being introduced into geological exploration, production and transportation of hydrocarbons.

Software solutions, combined with the introduction of multi-cluster drilling equipment, lateral extension and optimization of proppant flow rates in hydraulic fracturing, have already revolutionized the development of low-permeability reservoirs. Technological advances continue in this area, as well as in reducing energy costs and increasing oil recovery factor (ORF) for extra-heavy oils and kerogen, where surface retorting is increasingly being replaced by in-situ production technologies.

The desire to exploit aquatic resources as other reserves are depleted is driving the development of offshore and deepwater production technologies. In addition to offshore platforms, advanced subsea robotic production systems are increasingly in demand.

Companies are paying a lot of attention to methods of enhancing oil and gas recovery—different configurations of surfactants are being used, variants with thermal effects on the reservoir and injection of different types of gases, including CO2, are being developed.

In pipeline transportation, efficiency can be increased by improving the properties of the materials used, increasing the pressure, smooth coatings, anti-friction additives, and robotization of fault detection and repair processes.

In the processing of fossil resources, new solutions are being actively applied to increase the yield of the most valuable and expensive components and to adapt to changes in the incoming refinery feedstock. In some projects, good synergies can be achieved by processing refinery feedstock to produce higher value fuels and chemical products at the same time.

The traditional energy industry’s ability to provide a self-sufficient energy supply is expanding significantly. Equipment for the sustainable supply of facilities based on various fuels is becoming available: compressed natural gas, LPG, liquefied gas, coal, diesel.

Thermal power generation is also being improved, where the main efforts are aimed at increasing the efficiency of combustion in turbines, ensuring maneuverability of operation, and introducing systems for minimizing emissions.

5. Progress in Carbon Capture, Utilization and Storage Technologies (CCUS)

The low-carbon agenda, as well as plans for greenhouse gas taxes and carbon border payments, have stimulated research on CCUS, including as an element of “greening” fossil fuels and improving their competitive position in changing market conditions.

There are already point projects at production sites to capture CO2 and immerse it back into the reservoir to displace hydrocarbons. Oil and gas chemistry, refining, hydrogen production, metallurgy, the cement industry, and thermal generation are considered promising applications of CCUS technologies. However, so far everything is limited to the state of evaluation and experimental phase, primarily due to the high costs associated with the endeavor and the necessity for substantial enhancement of the elements of production chains, commencing from the capture stage.

The main challenges holding back the increased use of CCUS solutions are:

- large geographical distances between CO2 emission centers and acceptable storage sites;

- risks of environmental impact of CCUS processes due to the high carbon footprint of such production chains themselves and possible CO2 leakages after disposal;

- reduction of thermal generation efficiency when using CCUS processes due to high energy intensity of the process;

- the need to monitor and maintain CO2 storage facilities over long time horizons at a constant cost.

The viability of CCUS is contingent on its capacity to address the identified challenges and the prevailing costs of CO2 emissions, which directly impact the cost-effectiveness of the implemented solutions. Concurrently, advancements in technology will persist in domains external to the energy sector, where carbon dioxide emissions are an integral component of the production process. Consequently, novel solutions may experience an increase in demand within the energy sector over time.

Conclusion

The pivotal factors propelling the technological transformation of the energy sector include shifts in consumer demand, regulatory priorities, novel opportunities, and constraints arising from scientific advancements and the need to transition to more sophisticated production facilities. Concurrently, the energy sector itself is undergoing a rapid transformation, transitioning from closed fuel markets to a unified, interconnected competitive system.

Societal demands on energy systems are undergoing substantial transformation, precipitated by the emergence of novel categories of household and industrial energy-consuming equipment and vehicles. The transition towards a more electrified energy landscape is progressing steadily across all sectors of final consumption. The generation of electricity is becoming the primary domain of inter-fuel competition in the global energy sector.

In numerous countries worldwide, the cost of solar and wind power generation has fallen to a level that is competitive with that of fossil fuels. Concurrently, the development of other carbon-free solutions is underway, with the potential to penetrate specific competitiveness zones on a local scale. However, as the share of RES in the generation mix increases, system costs (backup, storage, grid infrastructure, etc.) and consequently energy prices for end consumers rise substantially. This underscores the need for a balanced approach that prioritizes both the availability of energy and its environmental sustainability.

The challenges associated with energy storage and accumulation assume particular significance within the context of carbon-free energy systems, particularly in light of the intermittent nature of renewable energy generation. Active research and technology development in this area are ongoing. At this juncture, it can be stated with a reasonable degree of confidence that lithium-ion solutions remain optimal in comparison to other alternatives for the majority of storage segments. However, the high dependence of batteries on rare metals gives rise to concerns, thereby prompting the exploration of alternative electric energy storage solutions. The optimal solution for each battery utilization segment varies, allowing multiple technologies to coexist and thrive. In the context of long-term electric power storage, particularly in cases where the generation is lost for an extended period, the carbon-free alternatives are limited to hydrogen. However, hydrogen is currently prohibitively expensive for large-scale applications. Consequently, reliance on fossil fuels for backup purposes emerges as a prevailing economic strategy for the time being.

The strategic integration of STP within the fossil energy sector will facilitate the sustained delivery of high production levels, even in the face of the depletion of readily accessible fields. Moreover, it will enable the provision of novel and more efficient energy supply solutions to consumers. Concurrently, gas and coal markets must adapt to operate within more stochastic frameworks, attributable to variations in RES production. It is important to note that fossil fuels and renewables are becoming not only competitors but also important complementary elements of a new energy system. This system should offer consumers both affordable and more environmentally friendly energy.

The ensuing decades will witness a period of intense technological competition across all segments of energy production, supply, and consumption. Concurrently, the global energy sector is expected to see a significant rise in trade, particularly in the domains of equipment and services. In this technological race, it is imperative not only to establish clear priorities but also to devise effective mechanisms for technological innovation, from theoretical frameworks to industrial production.

The ability to integrate into a shifting technological landscape, ensuring technological readiness for adaptation, will be a key factor in the competitiveness of companies and countries in this new era.

Bibliography

AEGIR, 2022. LCOE: update on recent trends (offshore). Available at: https://www.nrel.gov/wind/assets/pdfs/engineering-wkshp2022-1-1-jensen.pdf

Akbulatov, A.F. et al., 2017. Probing the Intrinsic Thermal and Photochemical Stability of Hybrid and Inorganic Lead Halide Perovskites. Journal of Physical Chemistry Letters, Vol. 8, No 6. P. 1211–1218. Available at: https://doi.org/10.1021/acs.jpclett.6b03026

Deloitte, 2023. How Companies Can Integrate ESG in Capital Allocation—and Why It Matters. WSJ. Jul 19. Available at: https://deloitte.wsj.com/sustainable-business/how-companies-can-integrate-esg-in-capital-allocationand-why-it-matters-a546a6c1

DNV, 2022. Energy Transition Outlook 2022: The Rise of Renewables. Available at: https://www.dnv.com/energy-transition-outlook/rise-of-renewables.html#:~:text=From%20today%20to%202050%2C%20wind,sees%20cost%20reductions%20of%2052%25

DNV, 2023. Energy Transition Outlook 2023. Available at: https://www.dnv.com/energy-transition-outlook/download.html

Environmental and Energy Study Institute, 2019. Energy Storage. February 2019: Fact Sheet. Available at: https://www.eesi.org/fi les/FactSheet_Energy_Storage_0219.pdf

EU Parliament, 2022. Press Release: Long-awaited common charger for mobile devices will be a reality in 2024. Available at: https://www.europarl.europa.eu/news/en/press-room/20220930IPR41928/long-awaited-common-charger-for-mobile-devices-will-be-a-reality-in-2024

ETIP OCEAN, 2020. 2030 Ocean Energy Vision. Available at: https://www.etipocean.eu/knowledge_hub/2030-ocean-energy-vision/

ETIP WIND, 2021. Getting fit for 55 and set for 2050. Available at: https://etipwind.eu/files/reports/Flagship/fit-for-55/ETIPWind-Flagship-report-Fit-for-55-set-for-2050.pdf

European Commission, 2021. EU Strategic Energy Technology (SET) Plan. Available at: https://setis.ec.europa.eu/implementing-actions/ocean-energy_en

Grushevenko, D., Kapustin, N., 2023. Modelling of energy consumption in the transport sector. AIP Conference Proceedings, Vol. 2552.

IEA, 2023. World Energy Outlook 2023 Free Dataset. Available at: https://www.iea.org/data-and-statistics/data-product/world-energy-outlook-2023-free-dataset-2

IRENA, 2023a. Renewable Power Generation Costs in 2022. Abu Dhabi. Available at: https://www.irena.org/Publications/2023/Aug/Renewable-Power-Generation-Costs-in-2022

IRENA, 2023b. Scaling up investment in clean energy technologies. Abu Dhabi. Available at: https://mc-cd8320d4-36a1-40ac-83cc-3389-cdn-endpoint.azureedge.net/-/media/Files/IRENA/Agency/Publication/2023

Karn, A., Raj, K Bhavana, Gupta, R., Pustokhin, D., Pustokhina, I., Alharbi, M., Vairavasundaram, S., Varadarajan, V., Sengan, S., 2022. An Empirical Analysis of the Effects of Energy Price Shocks for Sustainable Energy on the Macro-Economy of South Asian Countries. Energies. Vol. 16. Issue 1. Available at: https://doi.org/10.3390/en16010363

Kulagin, V.A. (ed.), 2020. Perspektivy razvitiya mirovoy energetiki s uchetom vliyaniya tekhnologicheskogo progressa [Global energy development perspectives considering the impact of technological progress]. Moscow: ERI RAS (in Russian). Available at: https://www.eriras.ru/files/monograph_2020_ed_kulagin_v_a.pdf

Kulagin, V. A., Grushevenko, D. A., 2020. Will Hydrogen Be Able to Become the Fuel of the Future? Thermal Engineering. Vol. 67. P. 189-201. Available at: https://doi.org/10.1134/S0040601520040023

Kulagin, V.A., Grushevenko, D.A., 2023. Vodorodnaya energetika: za i protiv [Hydrogen energy: pros and cons]. In: Ekologiya, energetika, energosberezheniye: bjulleten’ [Ecology, energy, energy saving: bulletin] / Ed. by Klimenko, A.V. Vol. 2 (in Russian). Moscow: PAO “Mosenergo.”

Lazard, 2023. LCOE Lazard. April. Available at: https://www.lazard.com/media/2ozoovyg/lazards-lcoeplus-april-2023.pdf

Lewis, A., Estefen, S., Huckerby, J., Musial, W., Pontes, T., Torres-Martinez, J., 2011. Ocean Energy. In: IPCC Special Report on Renewable Energy Sources and Climate Change Mitigation / Edenhofer, O., Pichs-Madruga, R., Sokona, Y., Seyboth, K., Matschoss, P., Kadner, S., Zwickel, T., Eickemeier, P., Hansen, G., Schlömer, S., von Stechow, C. (eds). Cambridge, United Kingdom and New York, NY, USA: Cambridge University Press. Available at: https://www.ipcc.ch/site/assets/uploads/2018/03/Chapter-6-Ocean-Energy-1.pdf

Makarov, A.A., Kulagin, V.A., Grushevenko, D.A., Galkina, A.A. (eds.), 2024. Prognoz razvitiya energetiki mira i Rossii 2024 [Global and Russian energy outlook 2024]. Moscow: ERI RAS (in Russian). Available at: https://www.eriras.ru/files/prognoz-2024.pdf

Makarov, A., Mitrova, T., Kulagin, V., 2020. Long-term development of the global energy sector under the influence of energy policies and technological progress. Russian Journal of Economics, Vol. 6, No 4. P. 347-357. Available at: https://doi.org/10.32609/j.ruje.6.55196

Moses, J. B. K., Oludolapo, A.O., 2023. The levelized cost of energy and modifications for use in electricity generation planning. Energy Reports, Vol. 9, Supp. 9. P. 495-534. Available at: https://doi.org/10.1016/j.egyr.2023.06.036

OPEC, 2023. World Oil Outlook. Vienna. Available at: https://www.opec.org/opec_web/en/publications/340.htm

VDMA, 2022. International Technology Roadmap for Photovoltaic. Results (ITRPV). Available at: https://www.vdma.org/viewer/-/v2article/render/78984725

1.jpg)